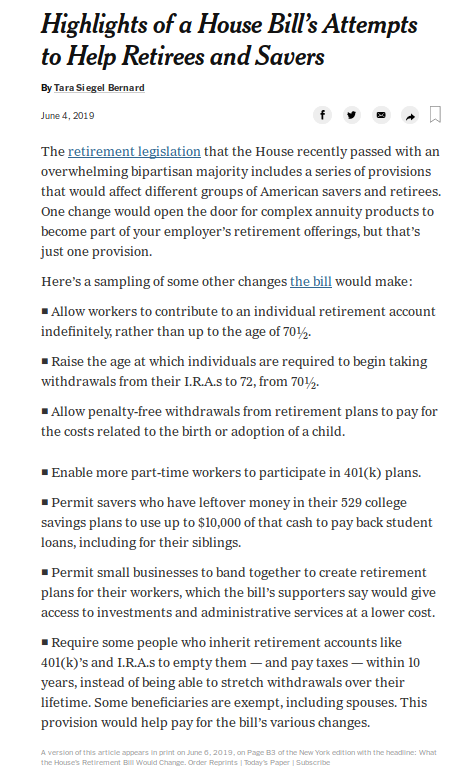

A large bipartisan majority of the US House of Representatives passed the SECURE Act. The bill has rule changes that many would welcome as well as some vexing provisions. The New York Times lists some of the bill’s highlights.

A large bipartisan majority of the US House of Representatives passed the SECURE Act. The bill has rule changes that many would welcome as well as some vexing provisions. The New York Times lists some of the bill’s highlights.

The otherwise relatively unobjectionable bill creates the potential of 401(k) investments being lost to badly managed or fraudulent annuities.

Section 204 gives a safe harbor to 401(k) plan sponsors who select so-called lifetime income products, another word for annuities, to appear among offerings to workers. This would mean that, if an employer picks an annuity provider and it goes out of business or rips off workers, they would not be able to sue the employer afterward. That could incentivize companies to find fly-by-night annuity providers that give good deals to the companies for business, making their money by ripping off the firm’s workers before filing for bankruptcy.

The lack of a safe harbor has been the primary hurdle to getting annuities into 401(k) offerings, said J. Mark Iwry, former senior adviser at the Treasury Department during the Obama years. “It’s the single most frequently mentioned obstacle by plan sponsors,” said Iwry, who is now a nonresident senior fellow at the Brookings Institution.

The piece by David Dayen at The Intercept describes the likely role of regulatory capture in the making of this imminent law. The Chairman of the House Ways and Means Committee is Massachusetts Democrat Richard Neal…

The annuities industry is a $235 billion-a-year business, with brokers enjoying kickbacks like resort vacations and luxury watches, according to a 2015 report from Sen. Elizabeth Warren, D-Mass. Insurance companies have longed to tap the trillions of dollars sitting in 401(k) plans for annuities.

That would include some of Neal’s biggest donors…

….

All in all, Neal picked up $30,000 last quarter in donations from companies and trade groups with a direct interest in the SECURE Act.

Then there’s Forbes contributor James Lange, whose hackles are raised because…

A more appropriate name for the bill would be the Extreme Death-Tax for IRA and Retirement Plan Owners Act, because it gives the IRS carte blanche to confiscate up to one third of your IRA and retirement plans. In other words, it’s a money grab.

Should you be concerned about “an IRA or a retirement plan that you were hoping you could leave to your children in a tax efficient manner after you are gone,” you’d best read his gory descriptions of the travesties of the SECURE Act. Mocking aside, if the beneficiaries of your bequeathments might have to rely on their inheritances, they’d be thankful for your attention to said tax efficiency.